Page 54 - Proceeding The 2nd International Seminar of Science and Technology : Accelerating Sustainable Innovation Towards Society 5.0

P. 54

nd

The 2 International Seminar of Science and Technology

“Accelerating Sustainable innovation towards Society 5.0”

ISST 2022 FST UT 2022

Universitas Terbuka

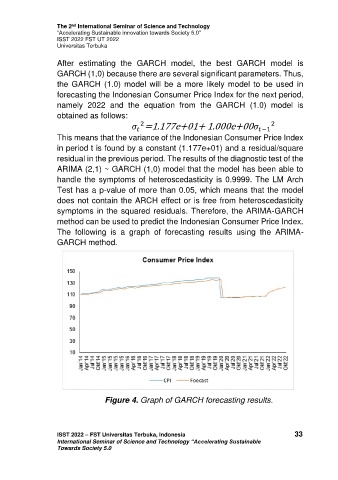

After estimating the GARCH model, the best GARCH model is

GARCH (1,0) because there are several significant parameters. Thus,

the GARCH (1.0) model will be a more likely model to be used in

forecasting the Indonesian Consumer Price Index for the next period,

namely 2022 and the equation from the GARCH (1.0) model is

obtained as follows:

2

=1.177e+01+ 1.000e+00 −1 2

This means that the variance of the Indonesian Consumer Price Index

in period t is found by a constant (1.177e+01) and a residual/square

residual in the previous period. The results of the diagnostic test of the

ARIMA (2,1) ~ GARCH (1,0) model that the model has been able to

handle the symptoms of heteroscedasticity is 0.9999. The LM Arch

Test has a p-value of more than 0.05, which means that the model

does not contain the ARCH effect or is free from heteroscedasticity

symptoms in the squared residuals. Therefore, the ARIMA-GARCH

method can be used to predict the Indonesian Consumer Price Index.

The following is a graph of forecasting results using the ARIMA-

GARCH method.

Figure 4. Graph of GARCH forecasting results.

ISST 2022 – FST Universitas Terbuka, Indonesia 33

International Seminar of Science and Technology “Accelerating Sustainable

Towards Society 5.0